Stock prices are up, inflation, so they tell us, down and volatility AWOL. When things get too far over the line, as they sometimes do, there's usually a correction or regression to the mean of sorts. The absence of fear, at least in markets, is almost always joined at the hip with the absence of common sense.

We recall in our many travels strolling into a noted chest surgeon's office some years ago to interview him and noticing a sign on the wall behind his desk: "There is nothing more uncertain or dangerous than a state of absolute certainty."

That pretty much sums up investor attitude about this market. The Fed apparently has convinced investors they won't be jacking up interest rates until sometime in 2015. And even then they'll raise them orderly.

Now what we don't hear--and this is our take on it--is any contingency for policy error. Most seem to take for granted the bureaucrats at the Fed will get it just right. The truth is they may already be behind the curve. Such things are usually only discerned in retrospect.

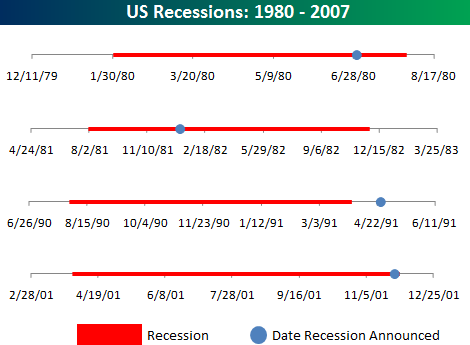

The Fed in the past has missed numerous recessions either going in or coming out. Truth be told, they usually miss them on both ends. In fact, the old joke about economists is they've correctly called nine of the last two recessions.

Note also that central bank bureaucrats every time they cut rates they claim they averted disaster. What they're really doing is causing it.

Now we don't want to trouble you with too much history especially since other than revisionists not too many today are interested. Harry Truman, the U.S.'s 33rd president, once noted, "The only thing new today is the history you failed to learn yesterday."

So just to bolster your confidence in government and bureaucrats, we'll close with three things here in America they run well: Amtrak, the Post Office and the VA Medical Centers.

What the chart below shows is the Fed missed on three of these four recessions, odds not much better than one would get in Vegas.