This deficit could be owing to many things like confirmation bias or just plain old linear thinking. But that 's for another time. Sinking oil prices the last couple years, to many, was expected to stay confined to that sector. Some research, however, shows that's not always true.

davidstockmanscontracorner.com/its-not-different-this-time-junk-defaults-spreading-beyond-energy

As noted below, apparel is a case in point. Most of us know about some of the larger retailers like Macy's and it plan to dump a bunch of jobs owing to poor sales and depressed earnings. But there is no such thing as a complete vacuum.

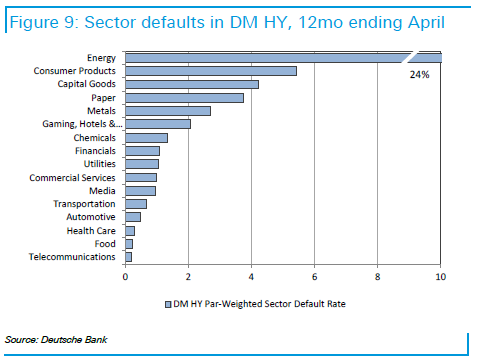

“Default cycles of the past have never been about a single sector, or small group of sectors,” Oleg Melentyev and Daniel Sorid, Deutsche credit strategiests, said in the note. “Yes, cycles were always driven by concentrated distress but they always found their way to affect other areas of the market.”

The strategists highlight recent pressure in the retail sector, including the travails of Quicksilver Inc., American Apparel LLC, and Aeropostale Inc., as evidence that defaults have already taken place outside of the commodities realm.

While pervasively low interest rates around the world offer some hope to the exceptionalists, by potentially helping to ease corporate funding pressures and allowing companies to refinance their debt. The European Central Bank’s planned corporate debt-buying program has helped boost already hefty demand for corporate paper.

Still, Deutsche reckons that this time the debt cycle isn’t that different.

“A frequent argument is being made here how all problems are going to stay limited to commodity sector,” the analysts concluded. “Evidence like this, coupled with emerging credit pressures in retail and capital goods sectors, suggest a contained cycle to be a weak starting assumption.”

No comments:

Post a Comment